What GameStop Says About Decentralized Finance

Pantera Blockchain Letter, February 2021

GAMESTOP

“What you get free costs too much”

— Jean Anouilh, French Playwright, 1950

“Free” trading apps like Robinhood aren’t free. They auction the ability to front-run their customers to the highest bidder. Hedge funds and High-Frequency Traders (HFTs) pay hundreds of millions of dollars annually to do just that. “Free” trading apps don’t work for their customers — they work for the hedge funds.

Ultimately their customers pay higher prices for their stock and receive lower prices when they sell. When the SEC charged Robinhood in December: “The order finds that Robinhood provided inferior trade prices that in aggregate deprived customers of $34.1 million even after taking into account the savings from not paying a commission.”

They got the 13th century tale backwards — robbing from the poor to give to the rich (hedge funds).

One wonders why the SEC allows that but not a bitcoin ETF. GameStop trades on only one exchange in only one country with just $67 million in average daily volume before the insanity. “Free” trading apps cutting off traders in the middle of trading sessions with no warning (fun to find out who wanted them to/forced them to cut off trading). Hedge funds paying to front-run retail investors.

Bitcoin on the other hand: Who can manipulate an asset that trades $70 BILLION a day on hundreds of exchanges in dozens of countries? Go figure.

GameStop is a colorful indicator of the tremendous desire for the decentralization of finance. Individuals are tired of centralized rent-seeking oligopolies controlling their financial lives. Tired of their value — in this case their private trade data — sold to the highest bidder.

This is the same underlying impulse in the rise of blockchain — and Decentralized Finance (DeFi) in particular. The power of the individual and open-source software over centralized for-profit companies.

There’s a very powerful new thing coming. Getting long blockchain is part of it — and a hedge against that uncertainty.

Decentralized exchanges like 1inch, 0x, Injective, Balancer, DODO, and Uniswap — are just code. They don’t front-run their customers. They don’t work for anybody.

The future is decentralized.

FUND PERFORMANCE

The power of this theme is emerging in the returns of our hedge funds. DeFi assets are out-performing even the remarkable performance of bitcoin.

We believe we are at the beginning of a multi-decade transformation.

Click on a Fund below for more information.

Please visit our website to learn more about Pantera and our offerings. If you need additional assistance, please contact our Capital Formation team at +1.650.854.7000 or by email at ir@panteracapital.com.

BEST-PERFORMING BITCOIN FUND

Pantera Bitcoin Fund is the best-performing bitcoin fund or trust in the United States. Low cost, no premium to NAV, guaranteed liquidity on any U.S. banking day, always at the Volume-Weighted Average Price for the day, no lockups, audited financials, and managed by a SEC registered investment advisor.

GAMESTOP & DECENTRALIZED FINANCE (DEFI) — BY JOEY KRUG

I love the recent GameStop story that’s been all over the news. For those who haven’t seen it, the short version is that Michael Burry (the Big Short guy) and the founder of Chewy (the online pet store company) took activist positions in GameStop earlier last year. So did a handful of Redditors, namely one guy named “Deep!@#$%&!Value” (you can take a guess), who’s been holding the position for a couple of years (he’d been buying call options on it).

Fast forward to January this year, and a ton of prominent hedge funds are short GameStop to the tune of about 140% of its float. You can see where this is going; GameStop was undoubtedly a company that was fading into irrelevance for a while. Still, it wasn’t going to zero in 2020 or 2021 based on their balance sheet. Many retail traders on WallStreetBets figured out that if they bought calls, hedging would push the price up, putting pressure on shorts and triggering cascading margin calls. It ended up causing a hedge fund called Melvin Capital to lose over 50% in one month. A lot of similar dynamics exist in cascading liquidations on crypto exchanges, which cause rapid price movements. It’s one of the reasons when we take risk-off, we usually do it by going to cash versus opening a short position. Crypto is so nascent and volatile it’s more like shorting GameStop if you were to outright short something. It has a high blowup risk vs. selling to cash or buying puts to hedge. Shorting quantitatively is something we will do as your risk is very different trading hourly vs. discretionarily, where something can blowup overnight if you’re holding a short position. The risk-reward isn’t there yet.

There’s a lot of other exciting dynamics surrounding GameStop here. I boil it down to three different things I think are notable. People on the internet can and are finding serious alpha with a midterm view that many of Wall Street’s best hedge funds didn’t capture. These users realized that shorting a stock when the company is already super beat up/oversold and has enough cash to keep kicking for a while is extremely risky. The equity behaves almost like a call option in these scenarios.

The second is that people realized that since over 100% of the float was short, they could merely squeeze the shorts by buying the stock. Those who remember the Icahn vs. Ackman Herbalife battle can see the resemblance here. However, on steroids, given the massive short interest here and the gigantic wave of retail buyers. To give you an idea, over *fifty percent* of Robinhood’s users were long GameStop, which is just super wild, and I think more than any other stock on the platform by far. People started piling in because they realized it was squeezing the funds who were short. Many users bought the stock, even knowing they’d eventually lose money as a way to “stick it to the man” because they feel like the financial system is rigged.

The third element is that brokers started limiting buys of the stock due to clearinghouses requiring more collateral to be posted. These increases were over ten times the typical collateral needed due to changes in value at risk due to the insanely high volatility of GameStop stock. This collateral needs to be posted mostly as an artifact of the existing system where the trade isn’t the settlement and settlement takes two days to occur. While a centralized database could fix this problem, there’s a massive coordination problem here and many misaligned incentive issues that make it seem unlikely that it’ll happen anytime soon, if ever in the traditional system.

What’s interesting here to me is that there is a massive overlap between the decentralized finance [DeFi] ecosystem and these themes. Since all of DeFi is open, anyone in the community can (and people do) share their views on where they believe alpha lies in the market. This chatter is widespread across Twitter, Reddit, and Discord groups across the cryptocurrency space. Sure, most of it is noise and has no edge, but someone posts something with an immense edge with a well thought out investment thesis once in a while.

The great thing about DeFi is that it’s global, has relatively low fees (once Ethereum scales), few intermediaries, transparent fair rules for everyone, and the trade is the settlement. It gets rid of the rigged system and replaces it with a shared public infrastructure that cannot be rigged. No broker can ratchet up collateral requirements because there is no gatekeeper broker. The clearinghouse is just a smart contract. Since everything is automated and happens via smart contracts, a trade either happens or it doesn’t. There is not + 2 days, but instead “trade intent” + 30 seconds. Once your trade gets confirmed on Ethereum, it’s final, and that’s it. And since these systems are global, anyone can access them anywhere in the world; it just takes a smartphone or computer and some cryptocurrency. The advent of DeFi mitigates the main problems and rigged parts of the system these Redditors were frustrated with.

When you use DeFi, you’ll realize finance is never going back. The moment I internalized that this was for sure the way the future is going was in 2020. This may surprise some people, given that I’ve been building in the DeFi space since 2014. But I was 90% confident for a very long time, and it wasn’t until last year when I became 99.9% convinced that DeFi is the future of finance. I wanted to trade from one asset into another. I had one cryptocurrency that was a token on Ethereum. I needed dollars to send to an OTC desk to get me a cryptocurrency from an exchange that didn’t trade in the US market. I used a decentralized exchange aggregator (a site that routes your order across dozens of decentralized token exchanges and gets you the best price) and traded that first token for USDC. The price I got was better than any OTC desk quoted me for the same trade. Ordinarily, I would’ve had to send it to a centralized exchange first, wait a while, trade it, and withdraw the USDC, which usually retakes a bit. Once I had the USDC, I sent the USDC to an OTC desk (at about 2 AM, when the banking system would’ve been closed). The OTC desk bought me the new token and then sent it to my wallet for that blockchain a few hours later.

So what just happened there is insanely cool. I’d have to sell the initial position in traditional finance, withdraw dollars after waiting for settlement, and wait for the wire to process (so three days so far). Then the foreign OTC desk could buy me the asset I needed. And I’d probably pay a fair amount of fees along the way too. And I certainly couldn’t have done it at 2 AM because nothing would’ve been open (neither my bank nor the market). Crypto markets trade 24/7.

Just the other night, I was getting indicative quotes on a 1000 ETH trade, and decentralized exchange aggregators offered lower slippage than Coinbase Prime. This feels like a watershed moment for the DeFi space. Not only is it a better system in theory, but it is also actually starting to become more useful to crypto users than other centralized systems. Companies like Coinbase will always help onboarding users to crypto from fiat/USD. Still, for crypto to crypto and stable coins <> crypto, DEXes will begin to dominate.

Ethereum is the asset at the forefront of all of this. Even after its recent run-up, it still trades at a P/S ratio of 40x, which will become earnings for ETH stakers when value switches to Ethereum 2.0. Revenue on Ethereum has grown over 400x since January 2020. It’s an insanely cheap asset compared to anything else in the public markets with that kind of growth relative to its revenue multiple. It’s not entirely crazy to see Ethereum being able to 5–10x from here, especially when compared to traditional equities markets. Ethereum is the base layer of this new open financial system. The vast majority of the value in that system is transacting on top of smart contracts written on Ethereum. The net present value of the global settlement layer’s transaction fees for all of finance is a considerable number. We have positioned the Pantera Liquid Token Fund around the opportunities surrounding decentralized finance and the Ethereum ecosystem for all the reasons above.

The fund was up 98% in January versus BTC up 15%. We think that similar to the last cycle, Bitcoin dominance (BTC’s percent of overall market cap in the space) will eventually go down into the forties again. In our view, the primary beneficiaries are likely to be Ethereum and Ethereum based decentralized finance assets, as well as eventually DeFi assets on other chains like Polkadot later in the year. This outperformance so far has mainly been due to our positioning surrounding DeFi (and some due to catching an opportune time to take some risk off after BTC hit $40k). These significant innovations we talked about above are only *4%* of the total cryptocurrency market cap. By the end of this cycle, we think they could potentially be 20%, or a relative outperformance of 5x.

On top of that, these assets’ underlying fundamentals should grow proportionate to the price of ETH. As ETH goes up, total value locked and volumes go up, which increases revenues, which increases the prices of these DeFi assets. As the market gains confidence that DeFi is here to stay and isn’t a fad, multiples will go up too, and things will begin to be valued by price/revenue/growth in DeFi. I think multiples could expand 4–5x across the board from here. As the protocols get more liquidity and their valuations go up, they also become more useful. There’s a massive recursive reflexive positive cycle of reinforcement here that leads us to believe DeFi is the best opportunity in the crypto space since Bitcoin and Ether themselves.

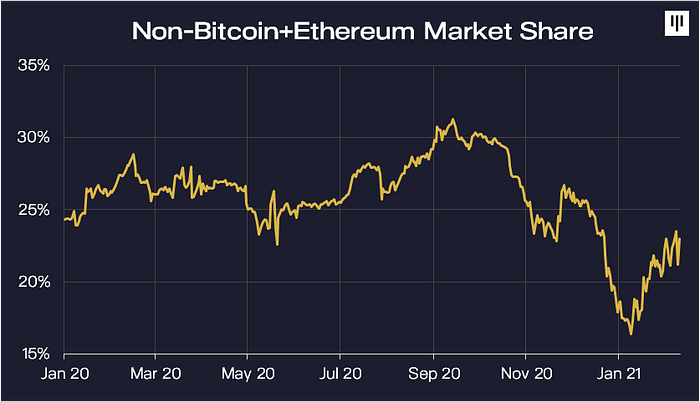

DECENTRALIZED FINANCE (DEFI)

As we wrote in our January investor letter, we’re very bullish on Ethereum. We’re even more bullish on the DeFi projects built on top Ethereum and Polkadot.

The non-bitcoin+ethereum market share has grown from 16% to 23% in the past 4 weeks. Watch this space. That’s where the largest gains are likely to be.

Pantera Liquid Token fund is currently long 68% non-bitcoin+ethereum.

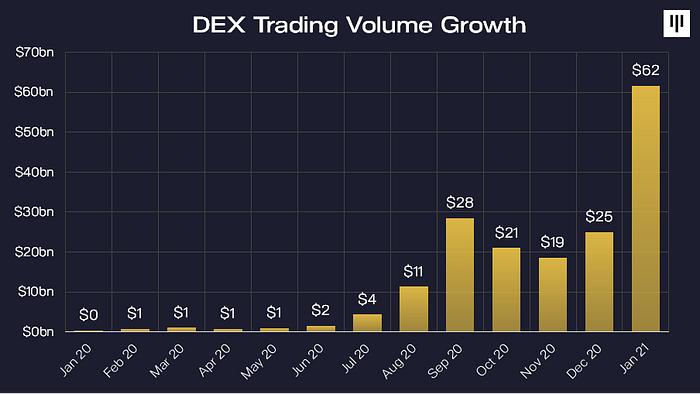

DECENTRALIZED FINANCE GROWTH METRICS

Decentralized exchange volume is beginning to take off. Total trading volume across DEXes surpassed $60bn in January 2021.

Pantera has positions in these decentralized exchanges:

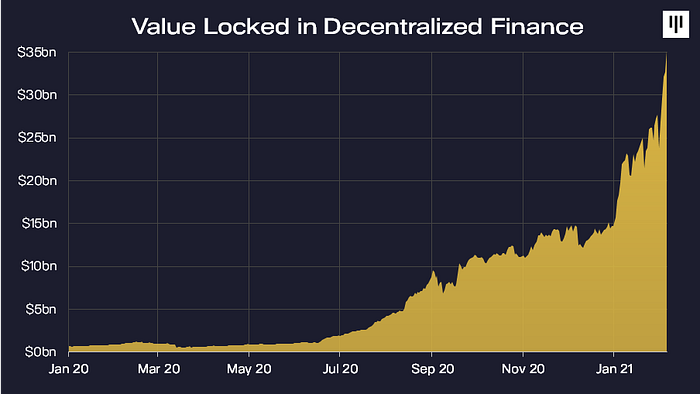

In parallel, the total value locked in DeFi protocols is continuing to rise. As of February 5th, the amount of value in DeFi was around $35bn. At the same time last year, it was just about $1bn in total.

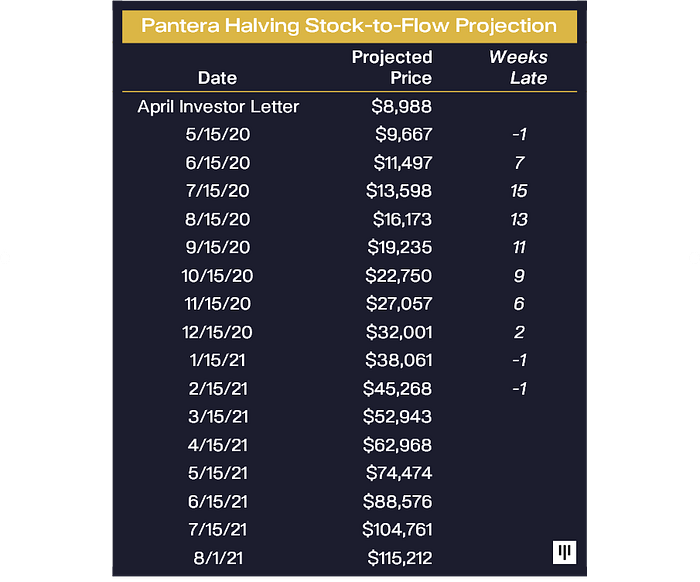

HALVING STOCK-TO-FLOW PROJECTION

Bitcoin is eerily on schedule. Exactly on our April 2020 investor letter projection — on pace for $115k by August.

ETHER FUTURES GO LIVE

The Chicago Mercantile Exchange added Ethereum futures. Another step in the institutionalization of the asset class.

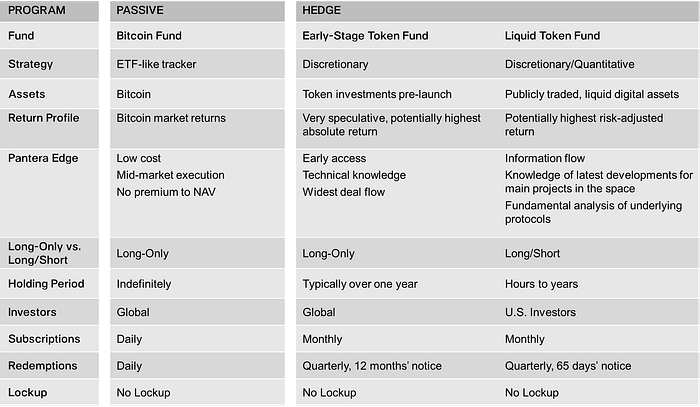

RENAMING TWO FUNDS

Our family of four funds sometimes confused new investors. “Which one does what again?” To clarify our strategies we’ve changed the names of two:

- Pantera ICO Fund is now Pantera Early-Stage Token Fund

- Pantera Digital Asset Fund is now Pantera Liquid Token Fund

It is important to note that there will be no change to the strategies of the Funds. The change is purely to make the fund names more self-evident.

RAT POISON

“Bitcoin is rat poison”

— Warren Buffet, 2018

I didn’t add that in the letter to take a snarky shot at such a legendary investor — I had ulterior motives…

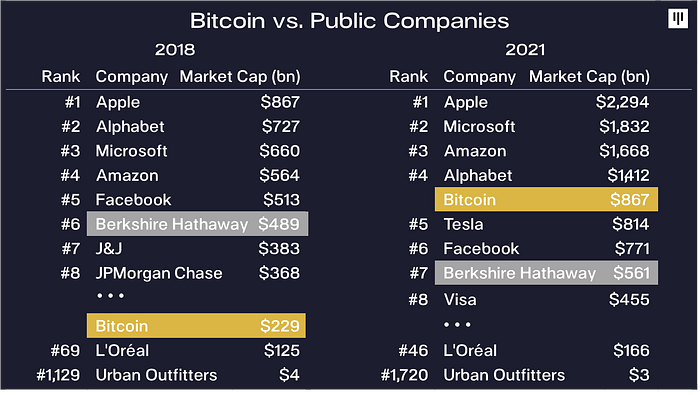

First, to put the scale of Bitcoin — as a proxy for the blockchain market generally — in perspective. Bitcoin itself is already bigger than all but four public companies in America.

If bitcoin continues at its 10-year compound annual growth rate it will surpass all public companies next year.

Second, to make a point about uncertainty. I’m not certain that bitcoin will go up. I believe IF it goes up, it will go up a lot. And, of course, it can only go down 1x. That’s an incredible asymmetry. In my opinion it’s the best expected value trade of my career. Warren Buffett first began public, negative statements about bitcoin in 2014:

“Stay away from Bitcoin. It’s a mirage”

— Warren Buffet, CNBC, March 14, 2014

Bitcoin is up 6,235% since then. Put another way: He would have to have been 98.5% sure it would go to ZERO to pass on a trade that has subsequently gone up that much.

But, really it’s the chance to share one of the best quotes of all time — Marc Andreessen’s reply when asked about that line:

“The track record of old white men who don’t understand tech crapping on tech they don’t understand still at 100%.”

— Marc Andreessen, CoinSummit in San Francisco, March 25, 2014

Take care everybody,

BLOCKCHAIN HEDGE FUNDS

CONFERENCE CALLS

Our investment team hosts monthly conference calls to help educate the community on blockchain. The team discusses important developments that are happening within the industry, and will often invite founders and CEOs of leading blockchain companies to participate in panel discussions. Below is a list of upcoming calls for which you can register for via this link.

- Thematic Call: Why Ethereum Is Undervalued, featuring Ethereum Co-Founder Joe Lubin :: February 16, 2021 9:00am PST

- Pantera Investor Prospect Conference Call :: February 24, 2021 9:00am PST

- Thematic Call: The Case for Blockchain Investment :: March 16, 2021 9:00am PDT

This letter is an informational document and does not constitute an investment recommendation, investment advice, an offer to sell or a solicitation to purchase any securities in Pantera Bitcoin Fund Ltd (the “Fund”) or any entity organized, controlled, or managed by Pantera Bitcoin Management LLC (“Pantera”) or any of its affiliates and therefore may not be relied upon in connection with any offer or sale of securities. Any offer or solicitation may only be made pursuant to a confidential private offering memorandum (or similar document) which will only be provided to qualified offerees and should be carefully reviewed carefully by any such offerees prior to investing.

This letter aims to summarize certain developments, articles, and/or media mentions with respect to bitcoin and other cryptocurrencies that Pantera believes may be of interest. The views expressed in this letter are the subjective views of Pantera personnel, based on information which is believed to be reliable and has been obtained from sources believed to be reliable, but no representation or warranty is made, expressed or implied, with respect to the fairness, correctness, accuracy, reasonableness, or completeness of the information and opinions. The information contained in this letter is current as of the date indicated at the front of the letter. Pantera does not undertake to update the information contained herein.

This document is not intended to provide, and should not be relied on for, accounting, legal, or tax advice, or investment recommendations. Pantera and its principals have made investments in some of the instruments discussed in this communication and may in the future make additional investments, including taking both long and short positions, in connection with such instruments without further notice.

Certain information contained in this letter constitutes “forward-looking statements”, which can be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue”, “believe”, or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual policies, procedures, and processes of Pantera and the performance of the Fund may differ materially from those reflected or contemplated in such forward-looking statements, and no undue reliance should be placed on these forward-looking statements, nor should the inclusion of these statements be regarded as Pantera’s representation that the Fund will achieve any strategy, objectives, or other plans. Past performance is not necessarily indicative of or a guarantee of future results.

It is strongly suggested that any prospective investor obtain independent advice in relation to any investment, financial, legal, tax, accounting, or regulatory issues discussed herein. Analyses and opinions contained herein may be based on assumptions that if altered can change the analyses or opinions expressed. Nothing contained herein shall constitute any representation or warranty as to future performance of any financial instrument, credit, currency rate, or other market or economic measure.

This document is confidential, is intended only for the person to whom it has been provided, and under no circumstance may a copy be shown, copied, transmitted, or otherwise given to any person other than the authorized recipient.